Australia will probably go to the polls next year, the American pre-primary debates will soon be underway, and politicians will no doubt be promising tax cuts, or at least promising not to raise them. In the last republican primaries in the US, there was a televised debate in May 2011when a group of Republican candidates stood in a row and declared they would not vote for one dollar in tax increases, even if they got ten dollars in spending cuts for it in negotiations with the president.

Most of don’t really want to pay taxes, but we know it’s a fact of life. We know that if a society is to function, somebody has to pay taxes, we would just rather it wasn’t us. However, even if we didn’t have the example of Greece in front of us, there are some basic rules of logic that tell us to be wary of politicians who refuse to raise taxes – ever.

The table below shows the levels of taxes of all forms of government for sixteen different economically advanced countries, the total spending and the difference, all as a percentage of GDP. Of course, the “difference” column isn’t necessarily the federal budget deficit or surplus, since some levels of government (say, a federal budget) may be in surplus while other levels (a state, or a city) may be in deficit or vice versa. But three countries do stand out as having a large gap between spending and taxes raised: Japan, (which has been bouncing in and out of recession for a very long time), France and the US.

| Country | Taxes | Spending | Diff |

| Australia | 25.8 | 35.3 | 9.5 |

| Austria | 43.4 | 50.5 | 7.1 |

| Canada | 32.2 | 41.9 | 9.7 |

| Czech Rep | 36.3 | 43.3 | 7.0 |

| Denmark | 49 | 57.6 | 8.6 |

| France | 44.6 | 56.1 | 11.5 |

| Germany | 40.7 | 45.4 | 4.7 |

| Italy | 42.6 | 49.8 | 7.2 |

| Japan | 27.6 | 42 | 14.4 |

| Netherlands | 39.8 | 49.8 | 10.0 |

| New Zealand | 34.5 | 47.5 | 13.0 |

| Norway | 43.6 | 43.9 | 0.3 |

| Sweden | 45.8 | 51.2 | 5.4 |

| UK | 39 | 48.5 | 9.5 |

| US | 26.9 | 41.6 | 14.7 |

| Unweighted average | 38.9 | 47.3 | 8.4 |

The interesting thing about the US is that its government spending as a fraction of GDP is a bit below average, at about 40 per cent. Yet it has the highest ‘difference’, because its tax collection figure is the second lowest. In other words, the US doesn’t appear to have a problem with ‘big government’. What it does have a problem with is ‘not enough taxes.’

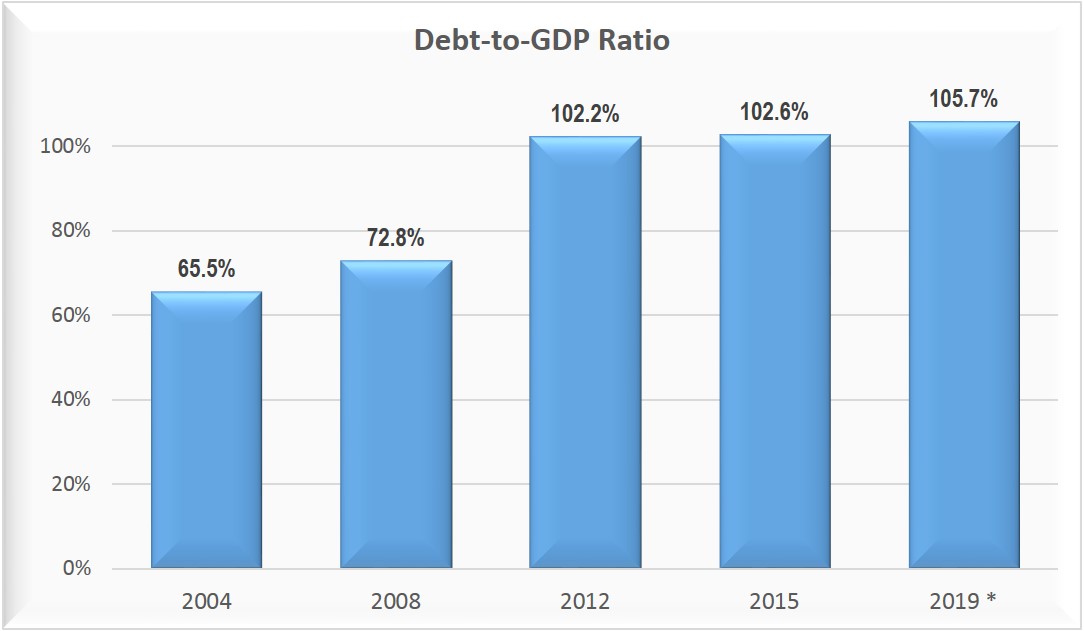

Of course, when a government spends more than it gets in taxes, its public debt rises. At present, the US has a total public debt to GDP ratio of just over 100 percent (A graph by Forbes is here, and a clickable, sortable table is here, but the graphic shows poorly in this page, so you might wish to follow the link.)

Of course, if a country wants to have world class medical and education systems, and first class infrastructure, these things have to be paid for. Talk about America’s ‘crumbling infrastructure’ has become common place, and a report by America’s civil engineers is here. On top of this, the wars in Iran and Iraq were put on the national ‘credit card’ (i.e., funded by budget deficits). Once it became obvious that the wars in Iraq and Iraq were going to take longer than a year, a tax measure should have been put in place to pay for them.

America also has the highest incarceration rate in the world, (about 4 times other advanced countries) and prisons cost money to run. The following quote from the ‘smart asset’ website actually did shock me:

“The American prison system is massive. So massive that it’s estimated turnover of $74 billion eclipses the GDP of 133 nations. What is perhaps most unsettling about this fun fact is that it is the American taxpayer who foots the bill…” [The figure refers to all prison, state and federal –RS]

In October 2013, the US government shut down for two weeks over a fight between the President and the congress over spending, taxes and debt levels. The rest of the world, especially holders of US government bonds got the jitters when it questioned if the American government would be able to pay it bills.

As it is, the US will probably go into the next election with all candidates promising ‘no tax rises, ever.’ This will only mean that the US will continue running budget deficits, although they are getting smaller as the economy recovers from the 2008 recession. A recent Forbes article sums up the current situation, but the last sentence is the most important:

The US budget deficit fell to about $US483 billion in fiscal year 2014, almost a $US200 billion drop from the previous year and the lowest level of President Barack Obama’s six years in office. The US Treasury Department released the official figures on Wednesday, generally confirming figures released by the nonpartisan Congressional Budget Office last week. It’s the smallest deficit recorded since 2008. FY2014 was the fifth consecutive year the deficit declined as a percentage of GDP. It is now an estimated 2.8% of GDP, a percentage that puts it below the average of the past 40 years. The Treasury’s figures chalked up the shrinking deficit to increased revenues from taxes and slowed growth in government spending. “It’s really a rise in revenues because of economic growth, because of the policies the president pursued, that we’ve made progress on the deficit,” said Shaun Donovan, the director of the Office of Management and Budget. The deficit has fallen sharply over the past few years, despite constant brinksmanship in Washington over raising the US debt ceiling. But concern about deficits has virtually disappeared from the campaign trail ahead of the 2014 midterm elections after being a central theme of 2010’s elections. “Politicians campaigning this fall have rarely raised the subject, not to mention the difficult prescriptions that are required to deal with red ink,” said Greg Valliere, the chief political strategist at Potomac Research Group, in a recent note. “No one wants to talk about the deficit.” [Emphasis by RS.]

It’s the last sentence that is the most worrying. If no politician is prepared to even discuss the deficit, no one is going to address the elephant in the room. Americans need to decide if they are willing to pay the taxes needed to live in a modern economy. And with a republican congress opposed to any tax increases, this seems unlikely.

Sometimes voting for politicians who promise ‘no tax increases, ever,” is just a slow and painful way of cutting off your feet, an inch at a time. Sooner or later there’ll be another ‘crisis’ over debt levels, and maybe another shutdown, and the rest of the world will have the jitters when it questions if the American government will be able to pay it bills.

Next week, some figures on Australia’s so-called ‘budget crisis’ that miraculously seems to have gone away in a sleight of hand trick: if it ever existed in the first place.